EVERY YEAR ABOUT THIS TIME, my blood pressure temporarily spikes in response to my anger. Anger about ever-rising health insurance premiums depleting our family pocketbook faster than a pick pocket.

I’ve vented and raged and spewed my discontent here. My jaw drops. My mind thinks a few unprintable words. My stress rises. How can we continue to pay these astronomical premiums and still have money for basic needs like food, gas, utilities, clothes, etc? I am thankful Randy and I paid off our mortgage decades ago, that our three kids are out of college and independent, that we’re OK driving aging (2003 and 2005) vehicles… We’ve always been, out of necessity, fiscally conservative, just as we were raised within poor rural families.

Let’s break it down. Health insurance premiums for my husband and me (I’m on his work plan) will go up $190 from $873/month to $1,000/month in 2018. That’s for each of us. Randy’s employer pays half his premium, $500. So we will shell out $1,500/month, or $18,000/annually. But before insurance kicks in, we must pay $3,600 each in deductibles. Alright then.

Let’s recrunch those numbers. In reality, our premiums are $1,300/month each if we need medical care and reach our deductibles. Times two, that’s $2,600/month or $31,200/year. Subtract the $6,000 Randy’s employer pays for his insurance and we’re down to $25,200. Still.

This year I met my $3,700 deductible. But I paid out $14,176 in premiums and deductible for around $4,000 (maybe a bit more; some bills haven’t processed yet) in medical expenses. I’m no math whiz. But even I can see that makes zero financial sense.

Holy, cow.

Somehow we’ve managed on a modest income, Randy’s as an automotive machinist and mine as a self-employed photographer and writer. But these latest insurance premium hikes are pushing us to a financial breaking point. I need to figure out an alternative to the $1,500 to be deducted from Randy’s paychecks each month for health insurance in 2018. Our incomes are not increasing to meet this through-the-roof expense.

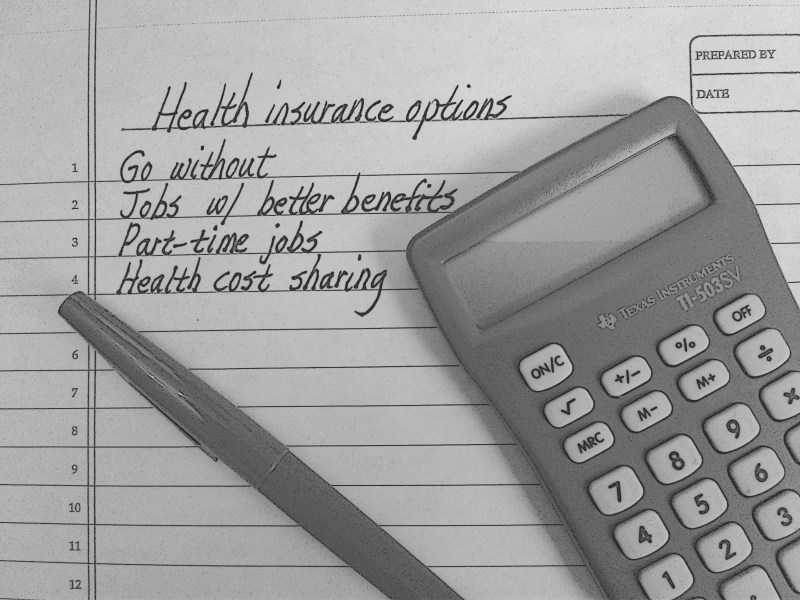

My kneejerk brainstorming produced the following options and reactions:

- Go without health insurance. Not a good idea given our ages and the financial risk.

- Find jobs with better benefits. At age 61, that’s unlikely.

- Take on second part-time jobs.

- Use a Christian-based health cost sharing plan. A strong possibility that requires additional investigation.

Our eldest daughter suggested we move to Canada with its publicly-financed healthcare. I know little about that system. But in a recent conversation with a Canadian visiting her brother here in Minnesota, I heard all about the shortage of doctors and the months of waiting to see one. Even if you’re seriously ill. No, thank you. Besides, I won’t move that far from my granddaughter.

There you go. Now, on to the research, the discussions, the continuing frustration and anger and stress and number crunching that each autumn overtake me.

I’ve joked with Randy that soon he’ll pay his employer to work because nothing will remain of his paychecks. I wish that statement didn’t feel uncomfortably close to reality.

#

AS BAD AS THE RATE HIKES would be for us, I know it could be worse. I’ve seen rates from a major carrier for individual off-exchange health insurance in my county of Rice and seven other southern Minnesota counties. If I chose the bronze plan (least expensive) with a $6,650 deductible, my monthly premium would be $1,361. Take that premium and deductible times two (there would be no subsidy from Randy’s employer) and our health coverage would cost $45,964 before medical bills would be covered. Holy cow. Who can afford that? Not us.

I realize many of you, especially self-employed small business owners or employees of small businesses, are dealing with the same absurd health insurance premiums. I don’t have an answer. I just know that the escalating cost of health insurance is creating a personal financial crisis for many of us. Additionally, because of those costs and matching high deductibles, we can’t afford medical care. Now does that make sense?

#

TELL ME: Are you dealing with/facing similar skyrocketing health insurance premiums? I’d like to hear about your situation and what you are doing. Are you going without insurance? Selected another option? Found a job with better benefits? Whatever you have done, or haven’t, I’m listening.

Please note that I moderate all comments. So please keep the discussion on topic and civil.

© Copyright 2017 Audrey Kletscher Helbling

Oh my – that is so painful. My husband has decent insurance and I use an HSA. It forces me to shop around and negotiate prices a bit. My employer will kick in some money to the HSA which helps. However I rarely use it – so far. It’s a nice way to save for when I need it though. HSA = zero premium. I just pay the whole thing up to a max (which is very high.

As a Canadian, I agree with your friend. Long, long waits for the simpliest things. Also taxes. Seriously, they’re really high comparably. When we left it was at least 55% income tax + sales/GST tax in Ontario was 15% = a lot of money.

My husband also has an HSA through work with some funds kicked in by his employer and some paid by him. He has not contributed the max, but we will reconsider. It’s difficult, though, when more and more of his paycheck is being eaten by health insurance premiums. We need money to pay for basic costs of living. We have been using HSA funds this year to cover our medical expenses. But those funds were not nearly enough.

I certainly don’t have any words of advice or wisdom at all. It is a concern for so many people and I am afraid that a lot of people have no option but to go without insurance which is not the answer at all. Hopefully your post will elect some helpful conversation.

That’s what I’m hoping for, some good discussion and valuable insight. Among seven couples we were together with the other night, three of us had major concerns about health insurance costs and the affect on our personal finances.

Thanks for opening the discussion Audrey. This is certainly discussed at our house. Just a few days ago we had a young man over to discuss a kitchen remodel- he’s like a son to us-and we all ended up yelling at each other about health care. I’d be interested in learning more about the Christian sharing programs. As for you- I suggest you start your retirement planning- SS and Medicare are not too far off. I’ll follow the comments here. Thanks

Yelling at each other in frustration about health care? A remodel of my 1970s vintage (picture a brown sink, leaky faucet and Formica countertops) has been on my wish list since we purchased our home in 1984. I realize now that will never happen. If not for the thousands of dollars we spent this year on health insurance premiums and medical bills, I could have a beautiful kitchen. Sigh.

I am checking into Medishare, a Christian-based cost sharing program, and have already spoken to at least one woman on the plan. She raves about it. However, the down side for me is that I would need to switch medical clinics (leaving the one where I’ve had care for 35 years) and the nearest hospital that accepts the plan is 25 miles away. If I need to be hospitalized, I want to stay at my local hospital. The plan also does not cover preventative care or pre-existing conditions (until three years after enrollment, as this woman told me). The website states clearly that this is not health insurance and that you are personally responsible for your medical bills (if the plan does not cover them). I’m making a mental list of pluses and minuses. The low cost of the monthly share payment (aka premium when compared to conventional health insurance) is incredibly low. The plan also fits my Christian values. I’m undecided and will continue investigating. It seems a possible affordable option, at least for me.

We are very, very lucky. My husband, myself and our daughter (who is not yet 26) are insured under my employer. The total premium is $1400 a month, of which my employer pays 75%. We have $300 deductible and 1800 max out of pocket per person. My daughter graduated and has a job in the Cities, but has chosen to stay on our plan because it is better insurance than what her employer offers. The health care industry/insurance is crazy and I don’t see anyone trying to do anything about it. People complained about the Affordable Care Act, and to be honest I don’t know much about it, but I give credit to Obama for trying SOMETHING. I don’t believe the people in Washington have any better plan in mind.

That is an excellent health insurance plan. I’m confused as to why some employers can get so much better rates for their employees than others. Does it depend on the size of the company and number of insured?

I understand and get frustrated, along with everyone else, over health care costs. It doesn’t seem right, especially when we drive by such luxurious insurance buildings and read what executives are paid.

That’s definitely part of the frustration.

Valerie, you are so right. Let’s face it – insurance companies are not in it just for the fun of it. It is indeed big business. I’m fortunate that we kept my husbands insurance plan when he worked for the government after he retired. I have Part A Medicare and the other is the same as if he were still working. After he passed I’ve been able to keep the same insurance. But one if my beefs is Long Term Care Insurance. We think we are doing a good job in putting out over $1500.00 a year per person for Long Term. Well let me tell you a story. Put it in a seperate savings account for that. We paid into LTC for over 10 years. When my husband got sick and we had passed 100 days, I called John Hancock to say just that. They informed me that the 100 days was having a person that they approved the company come in for 100 days. No family member. This means in cases like ours it could take years. In and out of the hospital we made about 12 days in four months. I told John Hancock that the $37,000 + that we had put into this I could if bought a new car. We thought we were planning for when we needed help. But we received nothing. Needless to say I dropped my policy right then and there. Medical Insurance is something we can’t live without, but people in small businesses are being over burdened just like Audrey and family. My daughter in Idaho is not on her husbands plan because she can’t afford what it would cost. My friend that was just here came from Canada. He was married to an American lady and they divorced so that he could return to his home country because of medical insurance. Yes, he has to wait sometimes, but feels it better than here. He could not afford insurance. He visits her some and they are still good friends. What a shame. I also know people here in the states that have divorced because of medical issues. When one is really in need and they can’t afford it, they are able to go on Medicade or one of the low income plans. What a sad sad situation.

Virginia, I am appalled at what I am reading in your comment. But not surprised. I am so sorry you dealt with this horrible situation regarding your husband’s care.

We pay through the roof on our insurance plan (well over $1,000) and get much less in return than we did before health care insurance became a national priority. It opened the door for a lot of corruption on the medical billing end and insurance premium costs. It has become such a cluster mess and the insurance companies have run amuck with higher costs and lower coverage. In my opinion, insurance companies should be nonprofits and medical billing of services should be consistent across the board. We live full-time in an RV on the road and we have run into a lot of pre-Medicare, self-employed couples who have chosen coverage in Christian-based healthcare co-ops or those that simply choose to take their chances and have found that it’s cheaper to pay medical costs than to purchase insurance–self-pay medical care and medications are actually cheaper than what they bill insurance companies. Its a no-win situation. 😦

Your final sentence summarizes the situation well: “It’s a no-win situation.”

I really have no clue what option we will choose. But thank you for your insights. I appreciate them.

That has to be anxiety inducing. As we are in open enrollment period this topic is especially timely.

I’m very thankful for the medical and other insurance coverage offered through my employer. In 2018, I will pay premiums of $373/mo for medical insurance for our family of four. Our total deductible is $3000 with out-of-pocket max of $4000 per person up to $8000 for the family. Our plan has an HSA with my employee contributing $700 annually (tiered based on salary) and I contribute additional funds. Our medical expenses thus far have been limited, but I know that can change instantly.

I wish you luck on whatever path you choose.

-Jocelyn

I am thankful you have such great health insurance and thus do not have those financial worries.

I am humbled to read your post and so many comments here. We chose a high deductible plan through Forrest’s employer so we pay no premium, but our annual deductible is 8K. There are too many variables to list here, but basically, it is a good plan if one doesn’t have a lot of medical expenses, and can use in-network physicians and facilities, and utilize certain labs and pharmacies. Forrest also contributes to an HSA, which we use a good bit. His employer also provides Wellness/Preventative tests and immunizations (routine physical), and limited mental health care at no cost. We are so thankful to be healthy and have not had any serious issues to confront in at least two decades.

As you know, I am all about prevention and discovering the crux of the problem. When we were kids, insurance was about covering broken bones or a trip to the doctor for the flu. Insurance was a benefit. Now it has become an industry that feeds off a nation that is ill as a result of decades of horrific lifestyles and the toxic foods we eat. It’s a huge problem – what we put in our bodies, what we breathe and put in the air and soil – it’s literally making us sick and killing us. Insurance isn’t the problem… the problem is what causes us to rely on insurance. We have to wake up and make serious changes.

Lori, I am thankful you and Forest have a good health insurance plan through his employer. I would take that $8,000 deductible with no premiums.

You are right that many health issues could be prevented by taking better care of our bodies. But not all. I missed a step, fell and broke my shoulder. Preventable? Perhaps. I still have no idea why I fell and efforts to get the local hospital (where my fall occurred) to cover my medical expenses through their liability coverage failed. Granted, I didn’t pursue it too hard. But accidents happen, bad health happens (no matter how hard you try to eat and live well).

I don’t even know if my parents had health insurance for us six kids when we were growing up. We seldom went to the doctor.

Your fall situation is certainly an “accident” and not preventable really. I’m talking more about diabetes, cancer, worn out joints (from obesity), stress – anything that stems from living a toxic life. I guess I’m saying if we could improve on prevention by educating and making changes, we might see a healthier America that did not need insurance like we depend on it now.

We didn’t see the doctor much as kids either. Mom was at home and she cared for us when we were sick. I think back then, all the folks had major medical in case something big came up, but otherwise we paid cash to the

Yes, much can be prevented. Unfortunately, education doesn’t necessarily work either. But that doesn’t mean we shouldn’t try.

Audrey, I replied to this but it disappeared! I wasn’t finished. Ha ha. Sometimes wordpress does quirky things.

Oh my you have hit a hot topic! The medical insurance industry is out of control in this country (in my opinion). My neighbor is a Canadian citizen married to a Us citizen living in the US. She cannot grasp why we as US citizen have and tolerate such a messed up health care system. Yes it’s true that for elective and non life threatening type medical issues she may have to wait a while but at least she doesn’t go bankrupt in the mean time. It is cheaper for her to travel by airlines to Canada and get medical exams/treatments than what it is in the US. My brother is a retired surgeon and has many times dealt with our corrupt, inefficient insurance system so much so that he too thinks that Canada has a much better system than we do here. What’s the difference between paying money out in taxes or pay money out in insurance premiums it’s still money out of our pockets but with taxes we have a bit more control if our elected representatives do their jobs, a big IF to be sure. There is no real control over insurance companies! Profits, profits, profits is their motivation!

I wish I had some good advice for you and your upcoming decisions. I too have to deal with the some problems you and most of us in the US have to deal with. Humm eat, keep a roof over our heads or pay and make insurance companies bank accounts bigger. Sometimes it appears to me that the insurance companies would rather see the older generations die off so that their medical risks are lower and thus profits larger, after all the insurance companies are all about rick management. What good is all of our medical advancements if nobody can afford them? Back in my growing up years my parents owned a small business and paid for 100% of their employees insurance. Why was this possible back then but impossible now?

Sorry rant now off. I too have looked into Medishare, a Christian-based cost sharing program however it does not apply up here, crummm. Perhaps it can work for you? I realize that you may be used to seeing the same doctor/clinic/hospital but sometimes changing is not all bad. Years ago my wife had a serious medical condition and kept going to the same doctor for over a year but she was never getting any better. Subsequently the doctor in question died unexpectedly and a new one took over her care. He told my wife and I that he wished to send her to the Mayo Clinic because they had newer updated procedures there, so away we went. Now years later I am glad we did or I may not have my wonderful wife around anymore. Moral of story her previous doctor was much older and thus set in ways and not open to new medical advances as her new doctor was.

Hummm in closing perhaps we need to form a nonprofit coop for medical care. Power in numbers……………………….

Thank you for ranting. You’ve given me some new info and more to consider. I expected this to be a hot topic and am glad readers like you feel comfortable sharing here. It doesn’t change anything, which is the unfortunate part. But at least we can vent and offer each other support.

One other thought. When we’re spending so much on health insurance, that money is not going into the economy to support businesses. So there’s a definite economic impact. I keep looking for ways to cut costs. I cancelled all my magazine subscriptions a few years ago. We ended our membership in the local arts center and attend fewer performances there. We certainly don’t eat out very often. Clothes? Thrift store shopping (I snagged a like-new wool pea coat for $8 recently). I buy on-sale. I’m really really cautious and conservative in my spending. I have not, though, cut back on giving to charity. I never thought at my age that health insurance would be my biggest financial issue to the detriment of the rest of our budget.

Your so correct on the economic impact. My niece is an officer at a major credit union and she told me that one of the major reasons for people filing bankruptcy are medical bills. In fact in that line of business they understand and even to a certain extent condone the practice after all what is a person supposed to do when they are priced out of the medical insurance markets and they get sick, die?

With high premiums, deductibles and cost of medical care, people make health choices every day based on finances. It’s to the point where only those with good incomes and excellent coverage (meaning the bulk of their health insurance premiums and medical costs do not come from their own pockets) are getting all the medical care they need when they need it. Every week I read a story or two or three in my local paper about fundraisers to help people in my community pay for medical and related expenses due to cancer or some other major health issue.

I am not at all surprised by your comment. The system is broken.

This is crazy, and I always feel horrible for this dilemma you face every fall. I can offer no words of advice here! Hope someone will be able to enlighten you with some different options.

Thank you, Jackie. We are not alone. Many others are facing the same problem of unaffordable health insurance premiums with high deductibles.

We did the math tonight. With rate increase from our current insurance, next year would cost the two of us $32,280 for the year, then ins. wouldn’t pay a penny until we each pay an additional $7,300 deductible. Or – change to a near worthless HMO and have to mess with the referral process. Neither my husband nor I have incomes. He took early retirement at 59 hoping to enjoy life, and I got hit with medical problems. I have many medical appointments every week, much of it being due to poor quality doctors. The whole thing has become a nightmare, and we have a few more years to live thru it. I think we’re going with the near worthless plan and use it when we can, otherwise go cash-based.

By the way, I am in Dallas TX. There were only a few insurance options here for individuals purchasing.

Thank you for sharing that because I wondered. In Minnesota, choices are more limited and costs much higher in regions outside the Twin Cities metro.

I understand your situation, hear your worry and financial concern. “Near worthless plan” seems a fitting description. Something must change. The cost of health insurance continues to financially devastate too many families. Like yours. Like mine.

Hi Audrey, I just saw this and thought of this post, so I thought I’d share it with you and interested readers!

Concerned About Health Care Expenses?

Join your friends and neighbors, watch a short video and have a conversation about healthcare.

A Documentary Film by Vincent Mondillo and Richard Master

FIX IT! HEALTHCARE AT THE TIPPING POINT

7:00pm, Monday, November 20, 2017

Community Action Center of Northfield

1651 Jefferson Parkway

Park and enter on north side of building; walk straight down the hallway to Meeting Room SS104

Free and open to everyone

Thank you so much for sharing this, Brenda. I wish I could attend. But I have something else planned for the same time. I’m still trying to figure out my health insurance. Thus far I’ve found nothing affordable.

The thoughts echoing in my mind are that of the freeloaders that we middle class support. Middle class family’s that work their butts off but barley make ends meet

The “barely make ends meet” frustrates me, especially at this stage of our lives. I was talking to two friends this weekend about health insurance costs. Both work in government. When they heard that our 2018 health insurance premiums will be $1,000/month each, they sat stunned. They had no idea, none, that insurance costs this much. When your employer covers all of your premium, I suppose you wouldn’t know and wouldn’t care. How many others out there have no idea the cost to those of us who are self-employed and/ore without our full premiums paid by employers?

I don’t think that anyone in our government really has a clue what it’s like to middle or lower class Americans

I agree 110 percent.