AS RANDY AND I DISCUSSED YET another issue with our aging vehicles over dinner, I glanced at the painting on our dining room wall. “Sometimes I wish we got around by horse and buggy,” I said. “Life would be simpler.”

Or would it? There would be horses to feed, wagons or sleighs to fix, manure to pitch from a barn we don’t have. And our travel would be limited. Nah, wouldn’t work.

So we continue to keep our 2003 Chevy Impala with 276,000 miles and our 2005 Dodge Caravan with some 175,000 miles in running order. Or should I say Randy does? He’s an automotive machinist (that’s different than a mechanic) and is pretty darned skilled in vehicle maintenance and repair after 40+ years in the profession. This year he’s done brake work on both vehicles, put a new sway bar in the car and replaced a belt tensioner and belt, alternator and radiator in the van. Oh, and done regular oil changes.

Randy’s skills save us lots in labor costs. But parts alone, even with his work place discount, still ran $865.

I figured with all those repairs already this year, we were good to go for awhile. But then Randy texted recently that the heater in the car wasn’t working. He had one long, cold 22-minute commute to work. He thought the problem may be a blown fuse. It wasn’t. And, not being skilled in the electrical components of a vehicle or wanting to navigate repair inside/under the dashboard, he let the guys at Witt Bros Service in Northfield work their repair magic. They’re a great, trustworthy crew, located across the parking lot from Randy’s work place. Still, sinking $200 (most of that in parts) into a nearly 18-year-old car gives reason to pause. But, hey, where can you buy a well-maintained used car for that price?

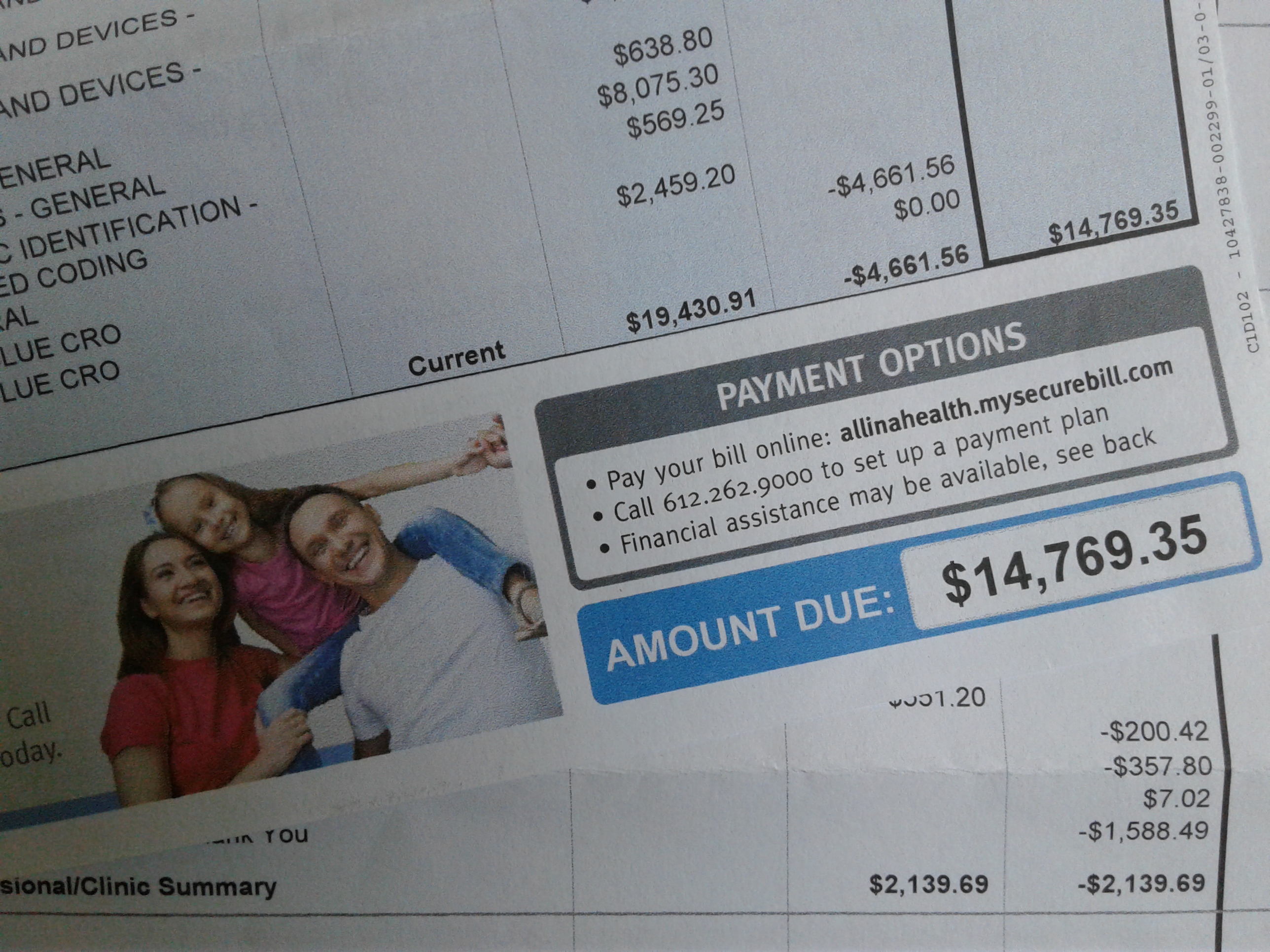

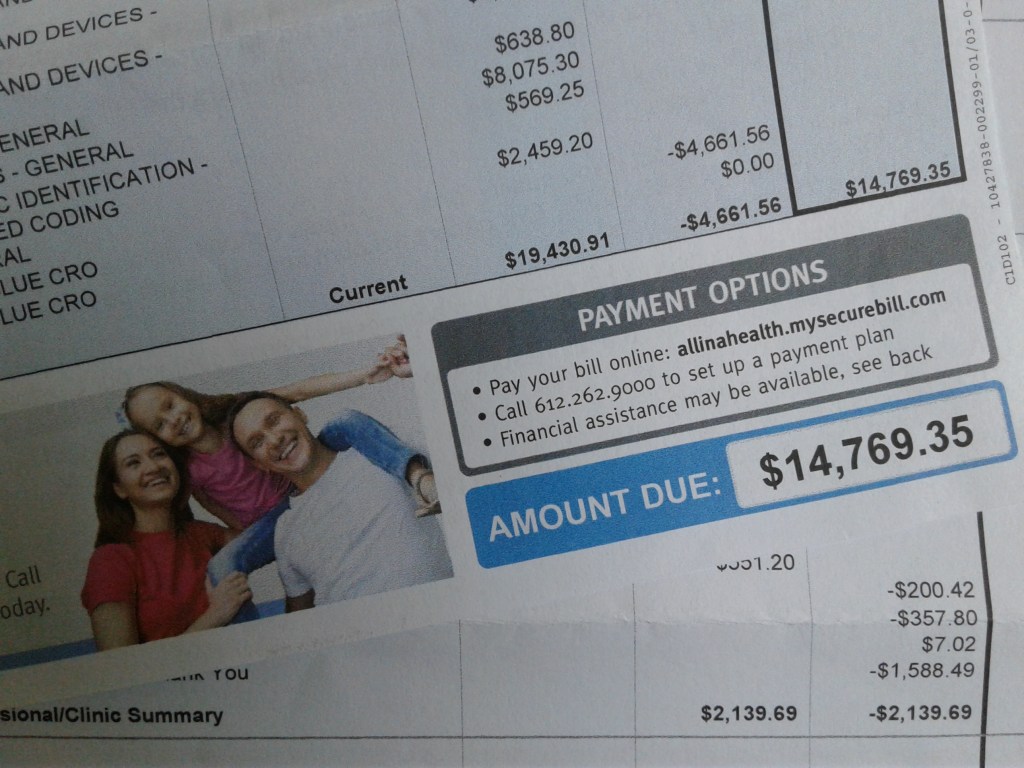

Now, if we weren’t paying $1,868/month in health insurance premiums in 2021 (up $144/month from this year), we could drive newer, nicer vehicles. Thus far in 2020, we’ve forked out $20,447 for health insurance premiums with deductibles of $4,250/each. Sigh. Nearly $21,000 could go a long way toward paying for a vehicle upgrade or anything for that matter. But, hey, at least we have health insurance (that is basically worthless unless we have a major health event) and wheels, not horses, to get around.

© Copyright 2020 Audrey Kletscher Helbling

Recent Comments