BACK ON MAY 22, gas cost $4.10/gallon here in Faribault. As the numbers on the pump scrolled up, finally locking at $64.50 for nearly 16 gallons, I felt a tinge of anxiety. My husband, Randy, commutes some 30 miles round trip to work in nearby Northfield. And at a time when he’d just learned that his job of 39 years would be cut at the end of August due to new corporate ownership, saving money was foremost on my mind. Still is.

Today I almost laugh at my reaction to that May pump price. Since then, gas prices have risen even higher to $4.73 in early June, now down slightly and holding steady at $4.69. Recent media reports, however, indicate fuel prices will continue to drop with the average national price currently at $4.63/gallon.

I haven’t done the math on how much more Randy’s commute is costing him this year. I do know, though, that I think twice now about out-of-town trips. Casual Sunday afternoon drives or drives simply to explore neighboring communities are mostly non-existent. It’s helped also that, since my mom’s death in January, we no longer need to travel 240 miles round trip to my native southwestern Minnesota. Not that gas expense would ever have been a consideration in visiting her.

And then there’s the cost of groceries. I consider myself a price savvy shopper who buys mostly basics, avoiding convenience foods. We eat simply and aim for healthy. But the price of chicken, our meat of choice, has skyrocketed as has the price of eggs. I cringe every time I see the grocery bill and feel thankful that I’m buying for only two rather than a family. One item I refuse to give up is the 4.4 ounces of dark chocolate (five individual servings) priced at $1.99. It’s my sole indulgence.

Dining out is, for us, an occasional treat. I can’t justify the expense when I consider the multiple meals I could prepare for the price of two restaurant servings. Recently, while vacationing in the central Minnesota lakes region, we ordered appetizers and two drinks at a channel-side restaurant. That cost us $47, tip included. When I remarked on the cost, Randy reminded me that we were on vacation. Still…

As we dined on that waterside restaurant lawn, I observed that plenty of people likely hold no money concerns. Pontoons and other expensive-looking boats glided in and out of dock slips at a steady pace. I felt a bit out of place here, our rusting 2005 mini van parked in the nearby crammed parking lot among all the newer vehicles. Our lives seem vastly different from those boaters and other diners.

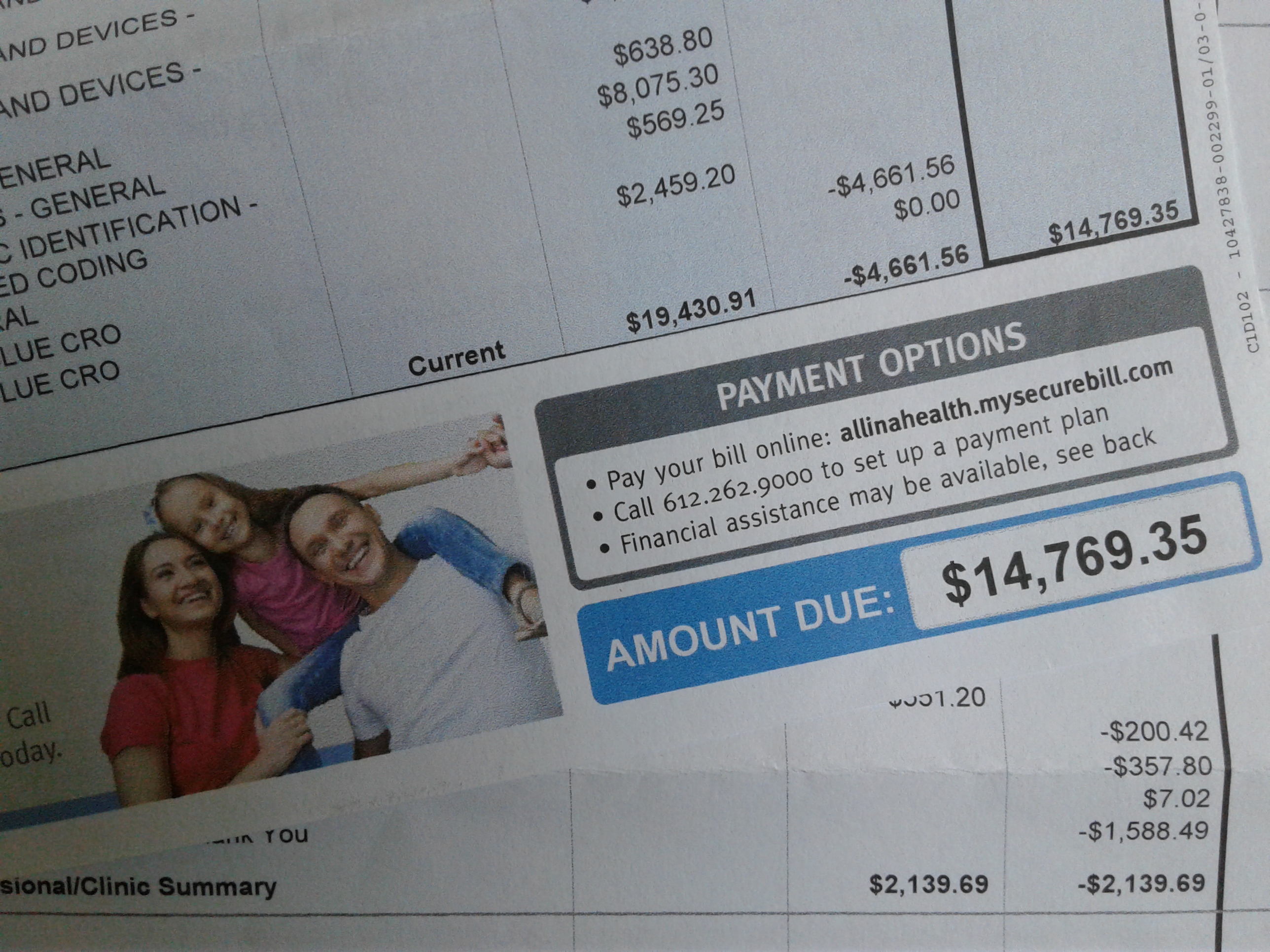

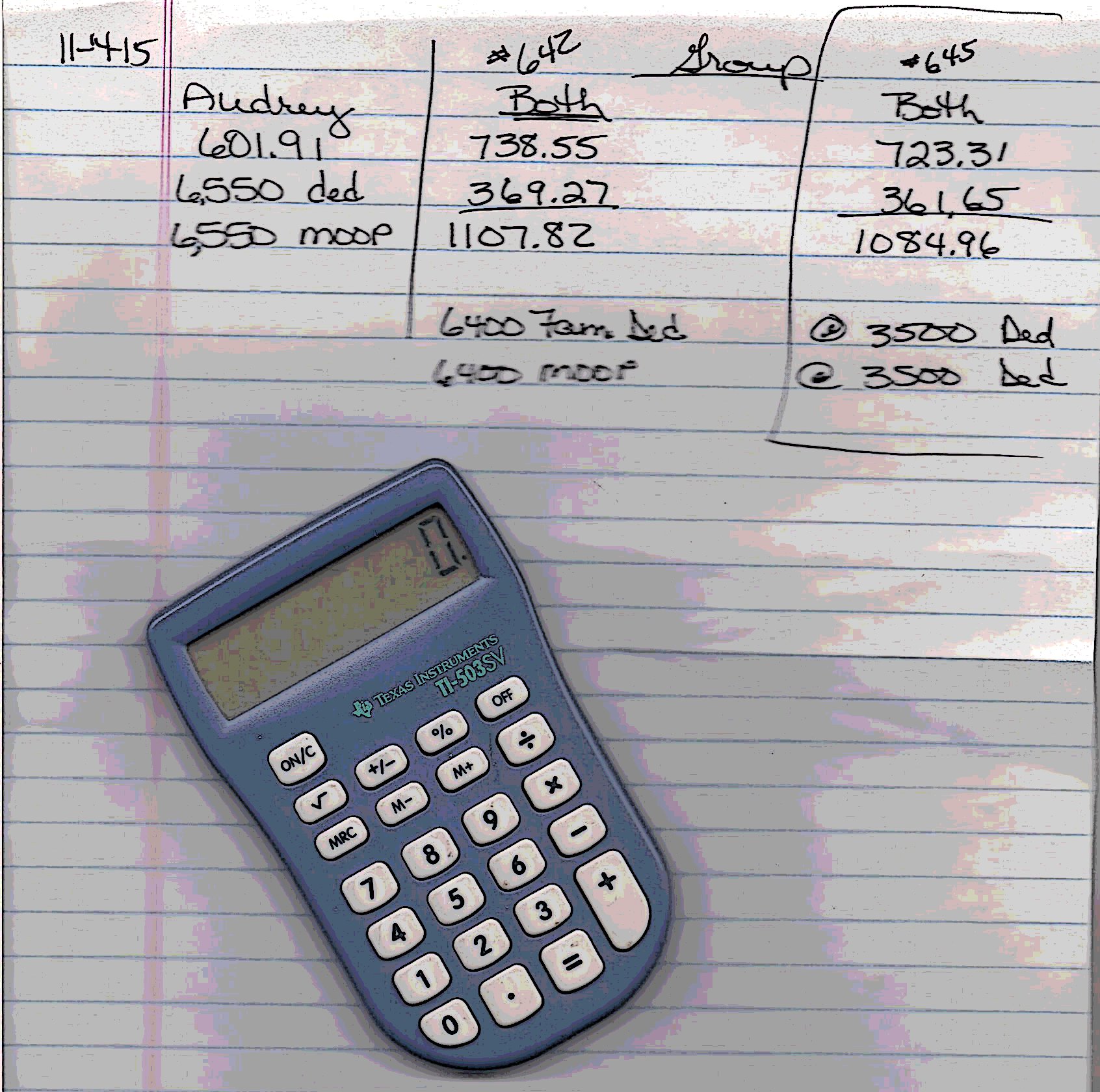

Yet, despite the economic disparities, I feel grateful. We are debt-free. We own a house. We are now both on Medicare, a mega financial savings after forking out some $20,000 annually in recent years for health insurance premiums for insurance we couldn’t use because of high deductibles.

I try not to dwell on the numbers in our retirement accounts, which show a loss of some $30,000 in the first half of 2022. It’s disheartening, especially as we close in on retirement. Our investment advisor advises us to hang in there, that the market will rebound. We don’t necessarily have the luxury of time. But at least we have retirement and personal savings accounts and are not struggling to pay bills like many Americans.

In all of this, I also feel thankful that Randy and I both grew up poor. Our approach to life and to finances is mostly similar. We don’t need the biggest, best, newest, because we’ve never had the biggest, best, newest. But we’ve always had enough.

TELL ME: What’s your approach to finances and inflation? Are you doing anything to cut costs?

© Copyright 2022 Audrey Kletscher Helbling

Recent Comments