I EXPECTED THE INCREASE. Yet, when I received notice of a $190 monthly hike in my health insurance premium, I reacted with shock. And anger. My new premium for an individual policy with a $6,550 deductible will be $602. Are you BLEEPING kidding me? That’s a 46 percent increase from my current $412/month premium. Plus, the deductible jumped $1,350 (from $5,200). For a “bronze” policy that basically offers only catastrophic coverage.

I EXPECTED THE INCREASE. Yet, when I received notice of a $190 monthly hike in my health insurance premium, I reacted with shock. And anger. My new premium for an individual policy with a $6,550 deductible will be $602. Are you BLEEPING kidding me? That’s a 46 percent increase from my current $412/month premium. Plus, the deductible jumped $1,350 (from $5,200). For a “bronze” policy that basically offers only catastrophic coverage.

I decided to let the news simmer. Maybe time would ease the sticker shock, the worry about extracting more money from an already tight budget. Perhaps I would accept this as simply the way things are under the Affordable Care Act. That hasn’t happened. I’m still mad. There’s nothing affordable about my health insurance premium.

But anger doesn’t solve problems. I needed to make a decision and stop thinking that I could just as well drive down the highway and toss $7,224 out the window toward the offices of a company that advises me in its ad campaigns to Live Fearless with a Trusted Name. Really? The cost of health insurance is now my biggest financial fear.

The health insurance issue wasn’t going away. So I scheduled an appointment with our accountant (who also sells insurance for the aforementioned company) to discuss options. She is as upset as my husband and me about the escalating cost of health insurance.

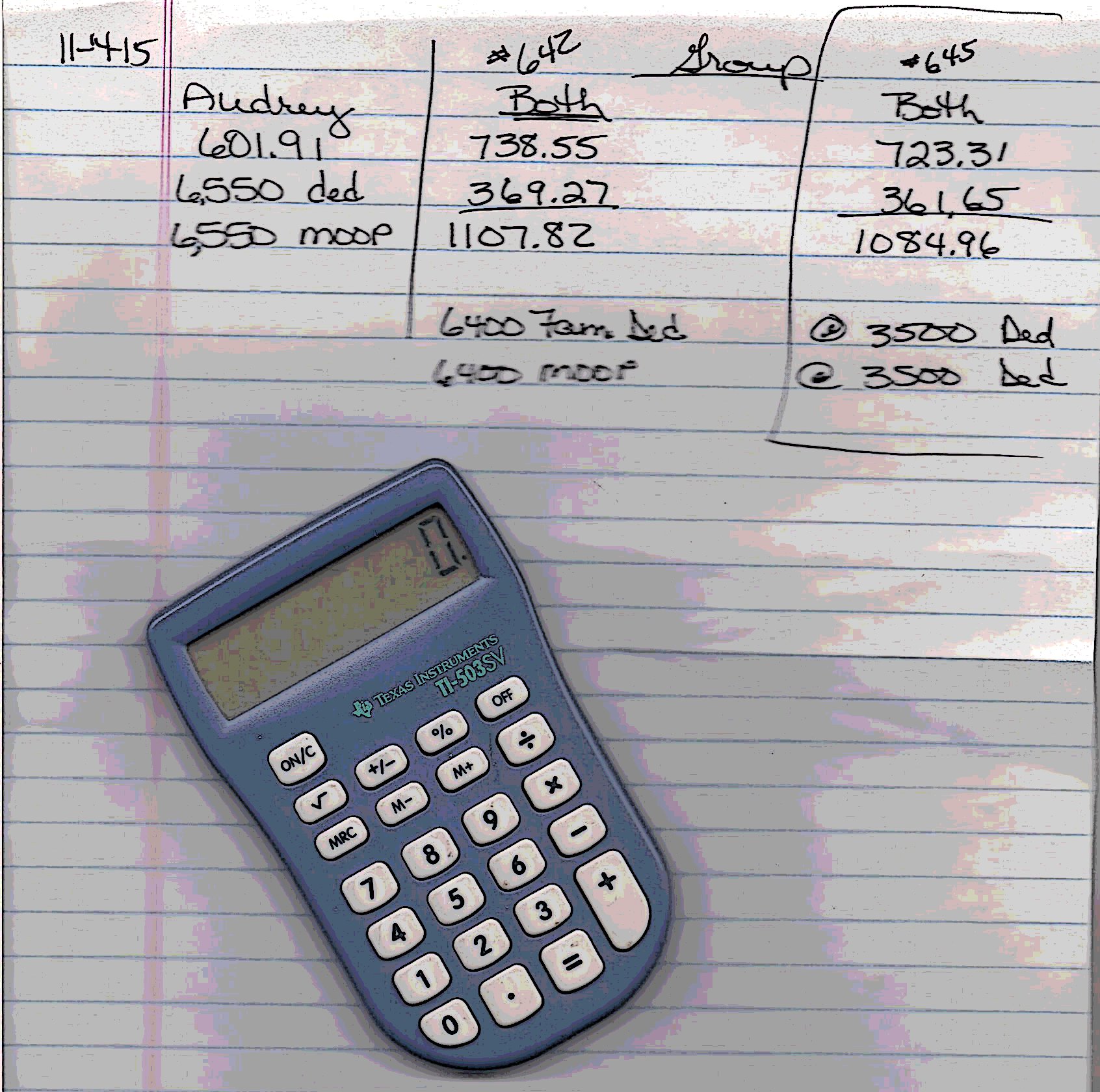

In three columns on lined paper, she inked in the existing options—stick with my individual plan or choose one of two plans offered through my husband’s employer. We inquired about other plans, too, and I later followed up by visiting the MNsure website to compare plans. Since my husband’s employer offers health insurance, we can’t get a subsidy anyway and it would be minimal if we could.

We settled on a $3,500/person deductible company plan with a $723/person monthly premium. (With the Live Fearless company.) It made the most sense given the premium and deductible differences and the impact on our taxes (which is why we saw the accountant).

My husband’s employer pays half of his premium. That $361/month will help.

I will now pay $723/month rather than $412/month. My health insurance in 2016 will cost me $8,676 compared to $4,944 currently.

Add in another $204/month for our college son’s health insurance premium and our family will fork out $1,288/month for health insurance premiums in 2016. (Keep in mind that the employer will add $4,332 to the pot, pushing the total annual premium cost to $19,788) Affordable? No. But I suppose one could argue that, if we need to use our health insurance beyond our $3,500 deductibles (for my husband and me) and rack up substantial medical bills, we will consider the $15,456 we paid in 2016 premiums well spent.

Health insurance, for us and I suspect many, has become basically a catastrophic plan that keeps us from going to the doctor.

Thankfully, our home mortgage was paid off years ago. We have income. Both of us grew up in poor families, therefore are thrifty. Yet, at this stage in our lives nearing retirement, we shouldn’t have to worry about out-of-control, astronomical health insurance premiums.

Something has to give here. With so much of our income now going toward health insurance, we are not spending elsewhere. Or saving for retirement. Like our tightening family budget, the economy will feel the impact.

GO AHEAD, VENT. Tell me your health insurance woes. Solutions are welcome. I know my family is far from alone in facing these excessive health insurance costs.

Click here to read a related story published on MPR.

© Copyright 2015 Audrey Kletscher Helbling

Dear Audrey,

This is also our biggest fear and sticker shock. We do not have our home paid off yet. We are actually trying to move back home, to Minnesota and work, I would like to be nearer my parents for when they may need me.

I am a voter and have asked all my medical care givers from the therapist to the dermatologist, what are we supposed to do? Why isn’t the medical field voicing their opinion and giving us, their patients, and the government options and answers for this, which I consider a crisis. Their livelihoods depend on it, they are losing business because people are opting to pay the penalty instead and not go to the doctor. The quality of care I feel has been degrading over the last couple of years.

Their answer is they don’t know. I ask if there is a stance taken by the AMA or other medical outlets such as American Journal of Medicine we may not be privy to that could tell us which way to direct our energies for change. So far they are as in the dark as I am.

My feeling is that it needs to be one of the major election issues, with answers, not “I plan to address” statements. I am worried for all of the people this is financially hurting, we cannot be saving all our money for health coverage. The government is talking about growing the economy and us needing to spend more and then taking it right back by allowing the health insurance to be out of control. It is a huge financial fear and a “catch 22”.

That’s all I have from my soapbox today. No answers, but I’m right there with you. I wish I had more options, more knowledge of where we go from here, less fear and anger at the state of things. But for now I will be happy knowing the conversation is still going out there with people I respect and that ask the questions that get us all thinking and sharing. I appreciate you.

Dear Janelle,

I appreciate your thoughtful response and your pursuit of this issue with healthcare providers. I wish I had the answers. I only know that SOMETHING MUST BE DONE, and soon. The thought has crossed my mind, too, of dropping health insurance and simply paying the penalty. Even though I’m in good health, I am nearing 60 and anything can happen health-wise at this age.

Continue to stand on your soapbox. Our voices need to be heard.

On a personal note, I do hope you are able to return to Minnesota soon. That you want to come back for your parents shows me how dearly you love and care for them.

I have been reading your posts regarding escalating health insurance premiums for a few years now and with every post, I’m shocked at the ballooning costs however not surprised. Obama gained votes by telling everyone he would make health care more affordable but like George Orwell’s ‘1984’, the opposite has been the result. I do feel for you, Audrey, with those steep and unacceptable increases; that’s an enormous financial burden. Sadly, things in Oz are only heading closer and closer to your situation in the US – premiums spiralling upwards way above inflation and there’s not a thing the little guy can do about it. I think our premium has risen by about 40% in the last 18 months xx

Charlie, I am sorry you in Australia are also now facing ridiculous increases in your health insurance premiums.

There’s nothing “affordable” about healthcare in the U.S. Nothing.

My wife’s premium went from $520 to $750 a month. That is a 50% increase. I am still on the State’s plan which has seen no appreciable increase. From what I read, the largest increases are in the rural areas.

It always annoyed me that the Affordable Care Act focused on portability and subsidies for low income families without addressing the greatest challenge in health care: cost.

You’re right about costs being higher in rural areas. I don’t understand that at all. Why should where you live make a difference in what you pay for health insurance premiums?

Rural people tend to be older and in worse health than city dwellers. Medical insurance is determined by the coverage pool one lives in. Apparently, part of the price of sending our children to town is the ballooning costs of medical coverage in rural areas.

You just enlightened me on this.

My family is in the same situation. We are farmers and pay for our own insurance. Our premiums are due to increase 65%. I have a family member who said his insurance through his employer is going down. ACA is a travesty and I, too, am looking for solutions.

Sixty-five percent increase! Words elude me. This is beyond ridiculous.

I feel your pain since I am also self-employed. My husband’s insurance premium, through his employer, will also drop slightly. I’m not sure it’s the same plan as he has now, though.

If you find an affordable solution, let me know.

Affordable Care Act is a misnomer. This was clearly the “Get Everyone Insured Act.” Insurance of any kind is organized crime in my mind. How much profit is enough for insurance company? They didn’t clear billions after paying out claims so they have to jack up premiums? If you use insurance, your rates are bound to go up. If insurance companies lose on their investments, your rates are bound to go up rather than affect executives bonuses. To make healthcare truly affordable, there needs to be more reform. One could argue (as you touched on) that if something terrible happened to you, if you only had to pay your out-of-pocket amount, then this would be potentially affordable only in terms of what you have to pay vs actual cost. What you have to pay may still not be affordable within your specific and often fixed budget.

I can’t say I disagree with anything you wrote here, Dan. Thanks for sharing your opinion.

Dan, I will not disagree about the role of insurance companies but the way hospitals are run is a disgrace. The NYT did an expose on the cost of a simple bandage…and not one hospital could come up with a consistent price or a rational explanation for the cost – but they did know that whatever they chose to charge would be passed on and not challenged.

There are plenty of villains – but we are also aging as a nation and that will spike costs.

So much to think about and discuss. Thanks, as always, for your enlightening input.

All great points. I was painting with a pretty wide and general brush. I agree there are plenty of villains. I get the aging nation bit. I do think though, that if the insurance companies truly wanted reform they could affect some change.

I agree, Dan.

It would be in the best interest of insurance companies to resist reform. They make money on the margins, if the cost goes up, they make more money. What they want is predictability.

We received a notice here a month ago that our monthly insurance premium would also be going up. Unfortunately we’ve not been notified as to the specifics such as cost of deductible. Etc. I now have to call and ask for that information to be sent to us. Health care I believe is one of the biggest rip offs we have..you need it, so clinics n hospitals can charge whatever and we are helpless. I had to have an MRI earlier this year. My regular clinic requested $967 up front. After contacting insurance company to determine my costs versus what they’d pay, they advised I check elsewhere, which I did. I was able to get MRI done and only be out of pocket, $350…big difference I say. Again, that’s our health system. Seems like we’re going to constantly be “shopping ” around for best price/service. For sure, not affordable!

When we’re in need of healthcare, we should not have to shop around. But it’s a good thing you did, obviously.

I am astounded that YOU would need to contact your insurance company about specifics in your plan.

The reason I contacted my insurance company was the facility was telling me my out of pocket charge was the $900+ and that i had to pay upfront! Then they stated they’d reduce price if i paid cash to $600. I was trying to verify what insurance would pay, versus what i had to pay. It was a mess as we couldn’t get facility to provide their assigned “code” so BCBS could verify charges. BCBS thought charges were excessive…this facility is one we’ve used for years. However, they’d been bought out the previous year and apparently new company was trying to make money. Needless to say, I no longer go there.

Oh, OK, I see. I have been trying for months to get a medical bill straightened out regarding in-network and out-of-network. Stress, stress and more stress.

My mind is BLOWN – CRAZZZZYYYY! Right there with you in going over it and over it and over it and then before we knew it the enrollment date was closing in on us to make a final decision – like cramming for a BIG Test. Plus we are in a new state trying to set up doctors, dentists, eye care – will they accept new patients let alone our insurance – at least this is a bigger area with plenty of options for health care professionals.

And who likes cramming for tests? Not me. Good luck in figuring out everything you need to in healthcare.

We have had to shop around for services over the past few years and will probably end up doing that here as well. The thing that really gets me up on my soap box is paying all these monies for care and the care available is below par to sub par for services and where those services are located at times too. It is pretty bad when you have to put a certain percentage down for a service and then having to beg for a payment plan to pay off the cost or slap it on a credit card and suffer the interest costs in not being able to pay it off right away. It can be a vicious cycle at times leaving you stressed out physically and financially.

“Having to beg for a payment plan” should not happen.

Stress is right.

welcome to the world of Obama Care. think the next time you are in the voting booth who you voted for in the last election whether a D or R if they voted to implement this cost lowering government health plan I suggest you vote for someone else.

Now there’s perhaps one concrete way we can make a difference. With our vote.

I know you are not Catholic, but have you contacted the Knights of Columbus and checked out their insurance rates and plan? With sympathy and prayer -Rena

Just checked online per your suggestion. As far as I can tell, the Knights do not offer health insurance.

The system is broken and causing horrific price increases to average families. Who in this world can have a price increase like that and call it okay? Would a retailer or grocer do that to their customers? It would be considered criminal. It’s okay to speak about it Audrey, that’s the only way it will change when we finally all get mad about it!

Thank you, Dee. You’re absolutely right, of course, on every point.

I am so sorry to hear about yet another increase…. It’s really crazy to hear the sums of what you are paying for health insurance. I hope and pray something can be done…. it’s just crazy that’s all I got to say!!!

“Crazy” would be a fitting word. So many others are in the same situation.

Thank you Mr. President… Ours went up too

How much?

Our deductible went up $400.00 and our maximum out of pocket went up $2000.00 I know that the amount taken out of Hubby’s paycheck went up too. He also got a raise that was enough to cover that amount with pennies to spare.

So thankful your husband got a raise to cover the insurance premium cost hike. My husband needs a raise also. It’s been a really long time since he got an hourly pay increase. I don’t want to embarrass his employer here, but…

Having recently endured a major medical condition and suffered through the insurance maze I can attest to the fact that massive reforms are needed to our health care system. Perhaps a nonprofit corporation that replaces a for profit corporation may help. I recall a recent situation where I live where a business started up an MRI clinic that was cheaper than the local hospital. The Hospital ( a national chain) didn’t like having the competition so they went to court to shut down the clinic. In the end the clinic had to shut down because the State requires a “Certificate of Necessity” for them to compete with an established medical facility. The state said they do not want too many medical facilities. Where’s the competition there to help keep cost down? Also the general population has some fault in prices. Too many people run to the “doc” for a minor ailment such as the common cold. I work with a hypochondriac and when I asked her why she was going to the doc 2 times a week she said “why not insurance pays for it!” Good grief she has no knowledge of how economics works! In the end we all pay a higher insurance premium for her overuse of medical insurance.

It’s scary to think of potential medical problems. I told Audrey the story and now the rest of you will know too. I thought I was in good health, no problems showed up in my medical exams, blood test etc., no family history of diseases yet out of the blue I suffer a heart attack because of a clogged artery to the heart. Talk about medical bills! I am still working my way through what is cover by insurance, what is copay, what is max out of packet etc.

Unfortunately life does not come with a guarantee or warranty!

That is quite the story about the local business opening an MRI clinic and then being shut down. I also agree with you on the overuse and misuse of doctor’s visits “because insurance pays for it.”

Thank you for sharing your personal experience here. I am incredibly thankful that you survived. You’re right. Life does not come with a guarantee. We must be thankful for each day we have on this earth.

The Affordable care act has only one truth. It is only an “act” when the people who forced this legislation consider it affordable and caring.

Good point.

Audrey,

The Affordable” Health Care Act has made insurance anything but affordable. At this point I will be looking at plans again but we may opt to pay the penalty and go without insurance once again.

At this point we have been better served by saving the money we would have paid for insurance that would have such a high deductible that we would still be paying all of our own medical costs, unless there was a major catastrophe.

I have written a few emails to senators and representatives and have not even received a response.

I am a nurse and honestly feel like the situation is hopeless. I’ve not had a raise in more than three years yet the insurance companies and health care industry continue to raise their prices.

I’m angry! I’ve worked in the medical field for 40 years, I’m close to retirement, and can’t afford health insurance. My husband is retired but too young for Medicare. This whole situation sucks!

How ironic that you have worked in the medical field for nearly 40 years but cannot afford health insurance. That is ridiculous.

I feel and understand your hopelessness. What can we do? Obviously, the emails were ineffective. Hello, are you listening, elected officials?

And, yes, this whole situation sucks. As much as I dislike that word, it’s fitting.

WOW! We just finished open enrollment through my workplace, and this comment thread makes me incredibly thankful and grateful for the cost of premiums and relatively low deductibles under our plan. Sometimes it takes a little perspective.

The cost of medical insurance is one of the primary drivers for a retirement delay for my parents. Just a couple more years and dad is eligible for Medicare.

Yes, I hope anyone who has good health insurance coverage through an employer does not take that for granted. It is a huge financial benefit.

I expect many who would like to retire are facing the same delayed retirement because of health insurance costs as your parents.

I about felt sick to my stomach reading about your insurance increase.. and then even sicker reading other’s comments. We do not pay a premium (my husband’s employer pays) and our deductible is 3K and after that it’s 80/20 (we pay 20% of medical expenses). We take advantage of his health saving account, socking as much away as he can. I do not know what we’ll face when my husband retires in 6 years. For now, we try really hard to maintain good health by eating well and keeping fit. We have not been to a doctor in more than a decade. I am VERY thankful.

This has been quite the discussion in the comments section, hasn’t it? My husband and I certainly are not alone in facing financial challenges due to the Affordable Care Act. And, yes, anyone with an employer who pays full coverage is fortunate.

I am so sorry to hear about yet another increase in your health insurance. This is definitely something that affects a lot of people and I wonder at the people who are “helped” by the new healthcare system. Why them and not you? I do not understand how a system can be helpful to some and so difficult for others. I am fortunately covered under Chris’s policy and yes–our coverage has gone up as well and it is difficult for smaller companies to be able to cover their employees with the escalating costs of healthcare. I have no answers at all. It is something that you really don’t want to have to be worrying about at this stage in life—your frugal living can only stretch so far. I wish I had answers . And maybe an extra million or two bucks to offer. 😦

Yes, lots of people affected. You’re right in pointing out this is also a burden to smaller companies. I’ve heard of businesses which have dropped health insurance plans and instead pay their employees X amount of dollars toward health insurance plans they buy on their own. That might be a better option because then, at least, the employee can be eligible for a possible government subsidy.

You’re right that frugal living can only stretch so far. How well I understand that.

As a farmer, we have to comply with nondiscriminatory rules. And I am fine with that. But here is what doesn’t make sense. I was willing to purchase the exact same policy my husband and I have for our one employee. Because non-discrimantory rules say you can’t discriminate in benefits – one employee can’t be treated any different. So I thought having all three of us with the same health insurance plan would satisfy that requirement. Guess what? Not good enough. We would have to purchase a group policy, which the premiums were significantly higher for a group of three than individual plans. You just can’t win on this one.

Ah, yes, I’ve heard all about that nondiscriminatory rule from my husband, after he asked his employer about simply paying X amount to employees for individual health insurance coverage rather than offering insurance.

What you wrote makes zero sense. Why would a group policy cost so much more? Can anyone out there answer that question.

I feel for you, Wanda, I truly do. Just look at these comments and read how many of us are in the exact same situation with unaffordable health insurance premiums. And this is just a small sampling of people…

Insurance companies continue to rip us off, as they have for MANY YEARS, and folks chalk it up to the only positive thing to happen in mass healthcare in the US for decades. Figures.

Since the ACA we’re one of the millions of folks who are actually able to GET insurance (I couldn’t before, I have asthma) and AFFORD it (our premiums have gone up, but no more than my husband’s had been going up between 2000 and 2010, an INSANE time of insurance profit)

It’s easy to blame the ACA, but that’s not the sole cause of the rate increases. We pay more for health care (and get less) than every other industrialized nation – why do we even NEED health insurance companies? Why not Medicare Part E (for everone?)

Yes, you’re correct. There are likely many reasons for the increases in health insurance premiums. I do like the fact that under the Affordable Care Act, those with pre-existing conditions can now get coverage. I was one of those who could not switch plans.

I’m not familiar with Medicare. But soon enough I’ll have to become informed. What about Medicare Part E makes it a good option for everyone? Remember, I know nothing about Medicare.

Thanks for adding to the discussion.

I think you are having an interesting discussion here. Let me point to a few things though…

#1 – The ACA’s intention was to get a handle on the uninsured. Prior to the ACA, insurance companies were dumping the people with the most need off the rolls. They made an artificially cheap pool. Now that they are required to accept those patients, they are struggling to find the business model that can work. United Health Care is leaving the exchanges because they couldn’t make enough money – said they lost $500 million on exchange business; however they did report $6.5 billion in overall profits. They are a MN company, but never participated in the MN exchange. A lot of problems with the ACA is that they still must depend on for profit insurance carriers to insure everybody.

#2 – It is hard not to notice that nobody is complaining about Medicare. Medicare has been a workable system for decades and it has forced carriers to accept reasonable charges for services. A number of Democrats have wanted to simply expand Medicare to everybody. It looks like a reasonable alternative.

#3 – Medicare Part D (which is separate from Obamacare and came in during Bush admin) is the prescription drug program. The biggest flaw here is that the government is forbidden from negotiating prices with the pharmaceutical companies. Drug costs have been skyrocketing as well as generic companies are now seeking bigger profits. Canada’s RX prices are much, much less because they HAVE the right to negotiate those prices. The reason we do not is because the pharma lobby was able to push a few Republican hold outs in the voting to press for this exemption.

#4 – Because the ACA has most people covered, hospitals are not losing as much money on unpaid emergency care. I believe that they have not passed this savings on to the consumers as yet, but I think they will have to in the future.

#5 – Because the ACA has guaranteed coverage even for people with chronic conditions, the law put in a provision that would help subsidize insurance companies during the transition – realizing that higher than expected costs would be the norm for the first few years. However, Senator Marco Rubion managed to partially block this provision and many insurance carriers have either dropped out of exchanges or increased premiums to offset the costs that would have been reimbursed from the government via this provision. Rubio brags about his role in this, but what he has really done is save government expense at the cost of higher costs to consumers.

These are just a few of things that get lost in the debate about health care. It is a complicated subject but people see the simple result – high costs; at least for the near term. Vermont experimented with single payer a few years ago – it failed, but only because they required that everybody be included – even Medicare and VA. In essence, the state was paying the costs that the Feds would have been happy to assume. Colorado is putting a single payer program on the ballot next year – and they are not making Vermont’s mistake. But there is already rumblings that national insurance companies are going to blitz the state with ads to stop this program.

Thought I would add a few more items for discussion. The debate will not end anytime soon.

You obviously are well-versed on the subject. I appreciate the insights I gained from your comment. Thank you.

I believe here in Minnesota there was always insurance for people. If you were not insurable, there was insurance programs available for those people. For those that needed financial assistance, there were programs for that too.