I EXPECTED THE INCREASE. Yet, when I received notice of a $190 monthly hike in my health insurance premium, I reacted with shock. And anger. My new premium for an individual policy with a $6,550 deductible will be $602. Are you BLEEPING kidding me? That’s a 46 percent increase from my current $412/month premium. Plus, the deductible jumped $1,350 (from $5,200). For a “bronze” policy that basically offers only catastrophic coverage.

I EXPECTED THE INCREASE. Yet, when I received notice of a $190 monthly hike in my health insurance premium, I reacted with shock. And anger. My new premium for an individual policy with a $6,550 deductible will be $602. Are you BLEEPING kidding me? That’s a 46 percent increase from my current $412/month premium. Plus, the deductible jumped $1,350 (from $5,200). For a “bronze” policy that basically offers only catastrophic coverage.

I decided to let the news simmer. Maybe time would ease the sticker shock, the worry about extracting more money from an already tight budget. Perhaps I would accept this as simply the way things are under the Affordable Care Act. That hasn’t happened. I’m still mad. There’s nothing affordable about my health insurance premium.

But anger doesn’t solve problems. I needed to make a decision and stop thinking that I could just as well drive down the highway and toss $7,224 out the window toward the offices of a company that advises me in its ad campaigns to Live Fearless with a Trusted Name. Really? The cost of health insurance is now my biggest financial fear.

The health insurance issue wasn’t going away. So I scheduled an appointment with our accountant (who also sells insurance for the aforementioned company) to discuss options. She is as upset as my husband and me about the escalating cost of health insurance.

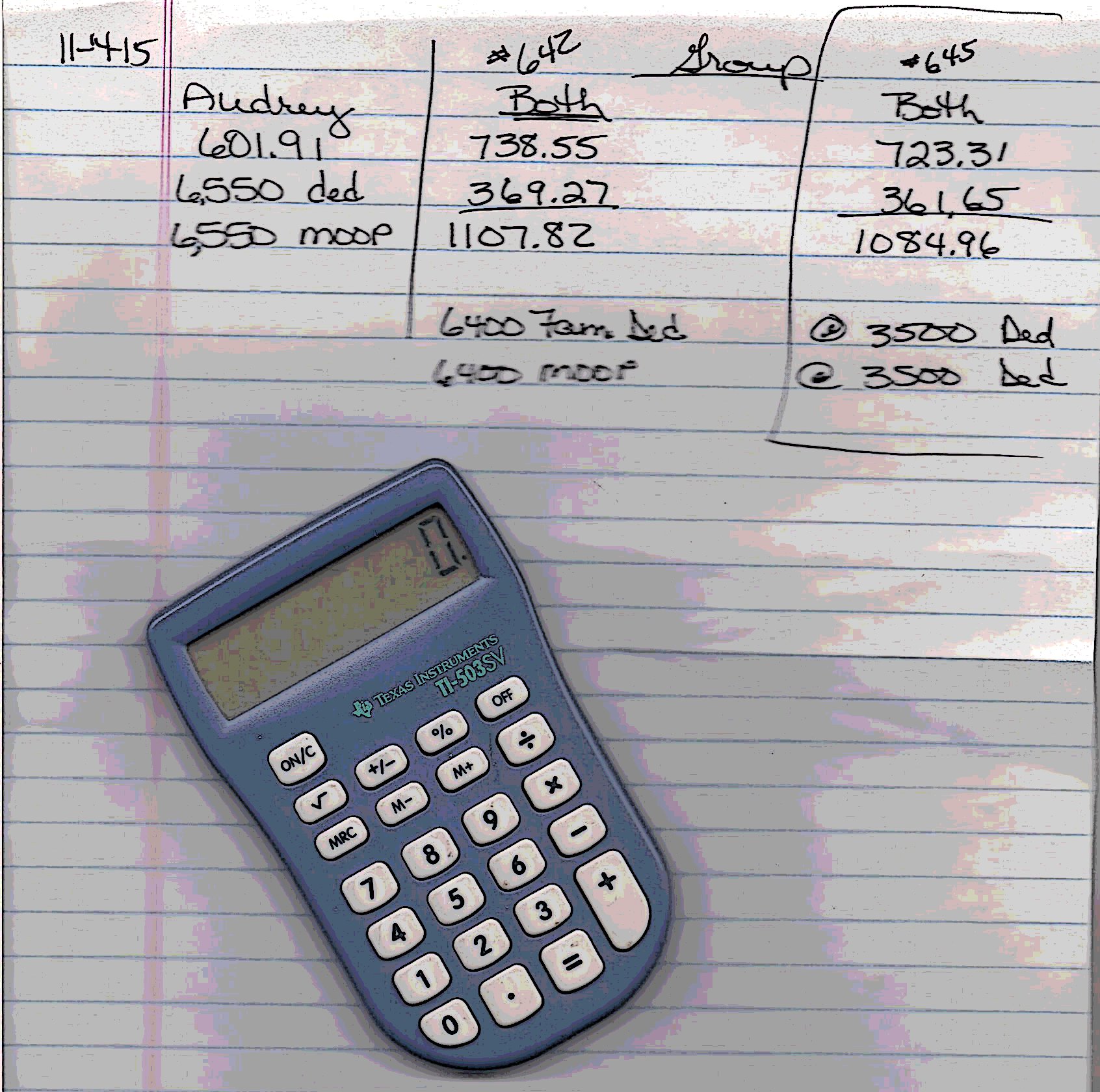

In three columns on lined paper, she inked in the existing options—stick with my individual plan or choose one of two plans offered through my husband’s employer. We inquired about other plans, too, and I later followed up by visiting the MNsure website to compare plans. Since my husband’s employer offers health insurance, we can’t get a subsidy anyway and it would be minimal if we could.

We settled on a $3,500/person deductible company plan with a $723/person monthly premium. (With the Live Fearless company.) It made the most sense given the premium and deductible differences and the impact on our taxes (which is why we saw the accountant).

My husband’s employer pays half of his premium. That $361/month will help.

I will now pay $723/month rather than $412/month. My health insurance in 2016 will cost me $8,676 compared to $4,944 currently.

Add in another $204/month for our college son’s health insurance premium and our family will fork out $1,288/month for health insurance premiums in 2016. (Keep in mind that the employer will add $4,332 to the pot, pushing the total annual premium cost to $19,788) Affordable? No. But I suppose one could argue that, if we need to use our health insurance beyond our $3,500 deductibles (for my husband and me) and rack up substantial medical bills, we will consider the $15,456 we paid in 2016 premiums well spent.

Health insurance, for us and I suspect many, has become basically a catastrophic plan that keeps us from going to the doctor.

Thankfully, our home mortgage was paid off years ago. We have income. Both of us grew up in poor families, therefore are thrifty. Yet, at this stage in our lives nearing retirement, we shouldn’t have to worry about out-of-control, astronomical health insurance premiums.

Something has to give here. With so much of our income now going toward health insurance, we are not spending elsewhere. Or saving for retirement. Like our tightening family budget, the economy will feel the impact.

GO AHEAD, VENT. Tell me your health insurance woes. Solutions are welcome. I know my family is far from alone in facing these excessive health insurance costs.

Click here to read a related story published on MPR.

© Copyright 2015 Audrey Kletscher Helbling

Recent Comments