From a Halloween display in Hayfield, Minnesota Prairie Roots file photo.

WHAT SCARES YOU? I mean really scares you.

Is it the current state of our political climate? Climate change? Changes in your personal life? Life that feels overwhelming? Overwhelmingly high health insurance rates?

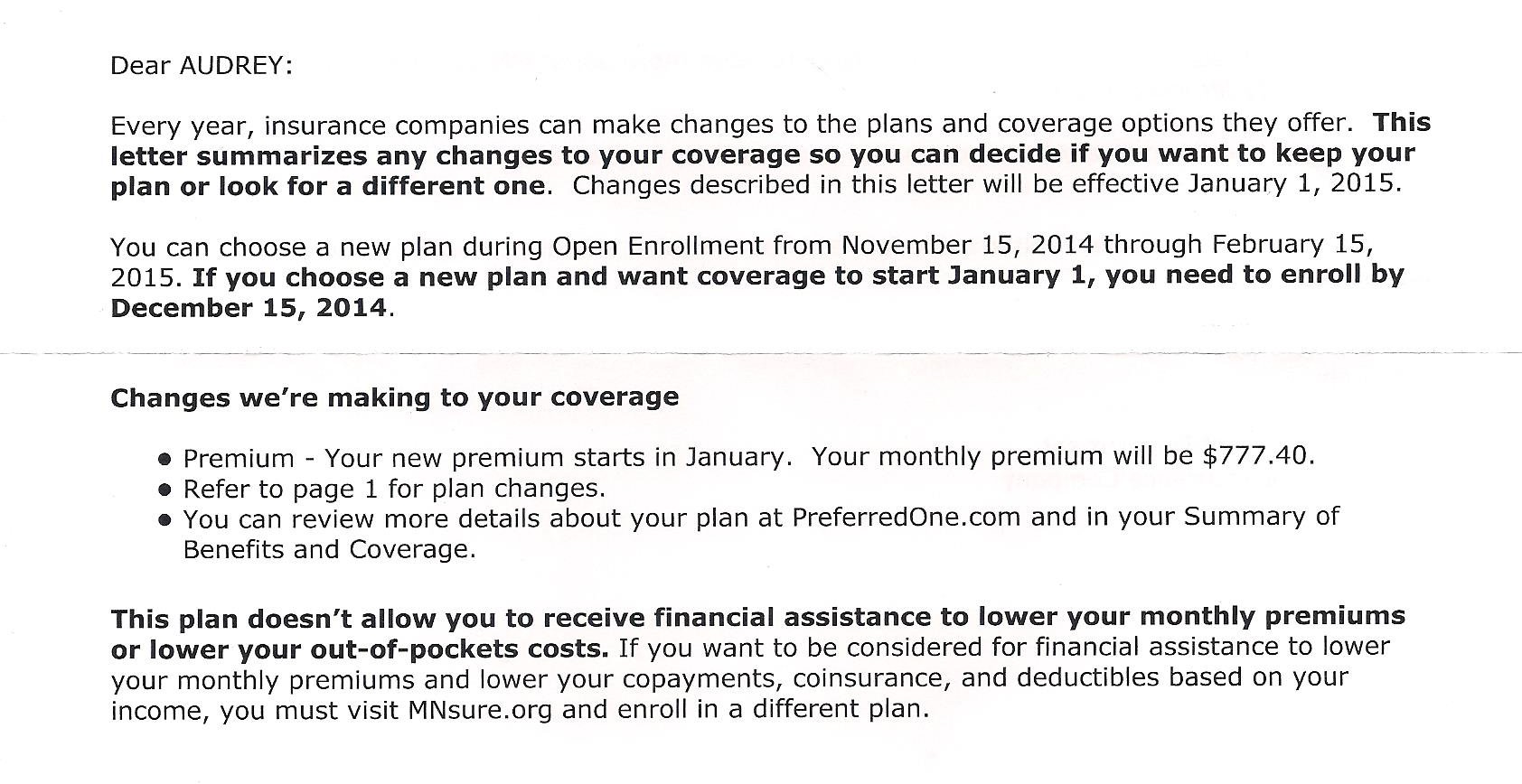

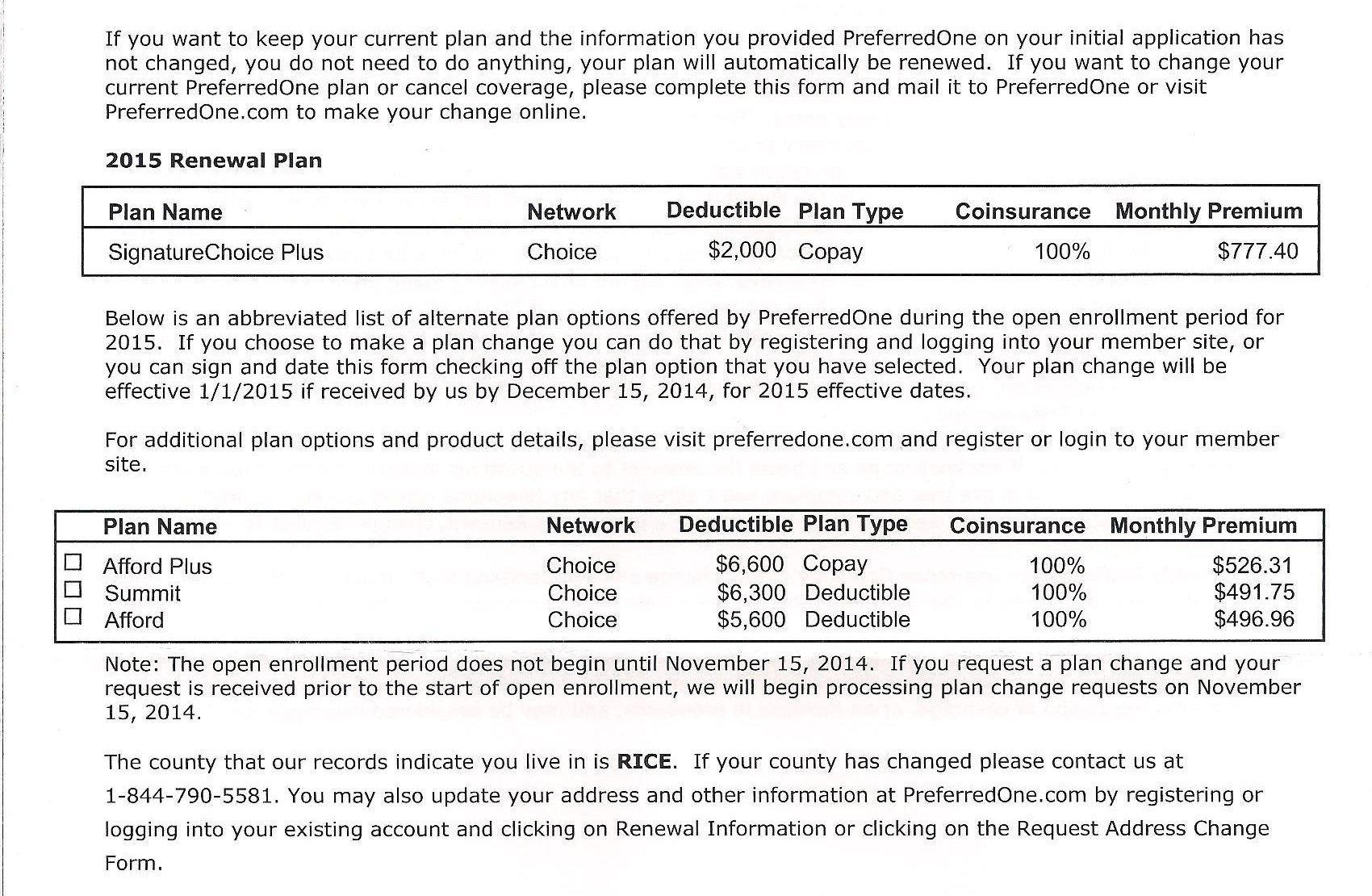

There’s so much to concern us. And I would place check marks in front of several items on that list, the most recent being health insurance premiums. Ours are increasing again. And I am seriously stressing about the additional $120/month we will pay for insurance that is nothing but a catastrophic plan. Our deductibles will rise from $4,000 each to $4,250 each come January 1.

I don’t pretend to be good at math. Words are my thing. But no matter that lack of skill set, I understand that the health insurance premium numbers are not good for our budget and have not been for years. I joke with my husband that he will need to pay his employer to work for him given the amount deducted from paychecks for insurance. Randy’s employer pays half of his premium, none of mine. I’m on Randy’s plan because I’m self-employed.

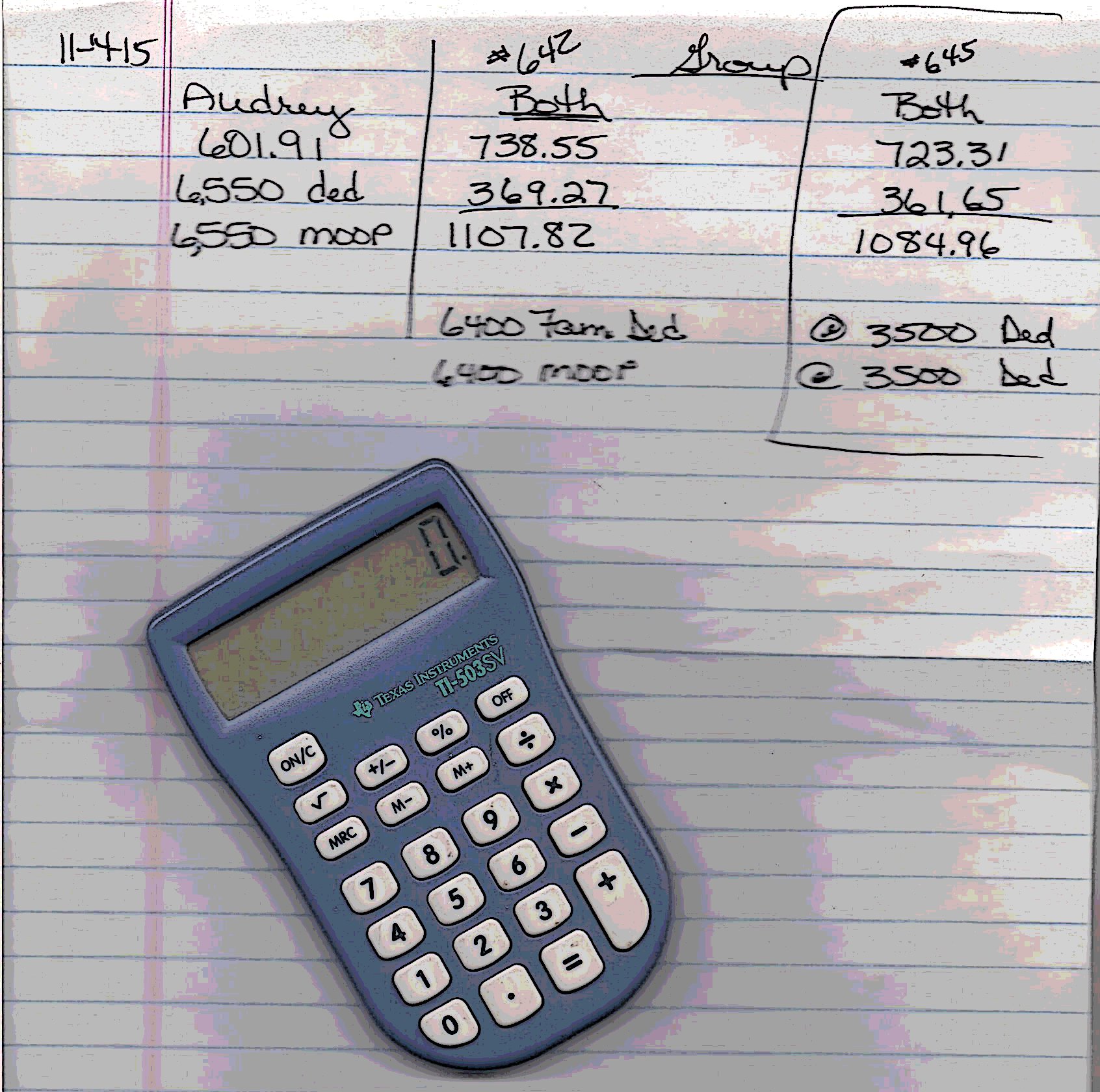

Now let me show you the numbers: In 2020, our monthly premiums will each be $1,149 for a total of $2,298 every single month. Of that, we will pay $1,723/month, which totals $20,677/year. And then we have those $4,250 individual deductibles before the insurance even kicks in.

This is absolutely absurd. There are no other words to describe the financial challenges we are facing because of health insurance rates that are through the roof ridiculous. No wonder we don’t go on big vacations, drive vehicles that are 15 and 17 years old, seldom dine out, have a vintage kitchen in need of a complete re-do, windows that need replacing, siding that needs paint or replacement…and don’t want to go to the doctor because we can’t afford to go to the doctor. Much of our income is funneled directly to the health insurance company rather than being pumped into the general economy. Sigh.

I never thought that at our age—in our early 60s—we would be in this financial situation because of health insurance premiums.

So what am I doing about this? Screaming, venting, crying, stressing. But I’ve also set up an appointment with a MNsure navigator to see if we qualify for any type of financial assistance. When I checked a few years back, that proved fruitless. I’m not especially hopeful this time either.

There you go, my financial horror story just in time for Halloween. I am thankful Randy and I both grew up in really poor families so we are not materialistic. We manage to pay all of our bills, get food on the table…and still donate to charities. We paid off our home mortgage years ago and I’m thankful we did.

But we never expected this overwhelming financial burden as we looked to the future and are nearing retirement.

This Halloween I’m not scared of things that go bump in the night. I’m scared of health insurance premiums.

THOUGHTS? Do you have similar health insurance horror stories?

© Copyright 2019 Audrey Kletscher Helbling

Recent Comments